Written by

Written by

- The Savvy Promise

At Savvy, our mission is to empower you to make informed financial choices. While we maintain stringent editorial standards, this article may include mentions of products offered by our partners. Here’s how we generate income.

In the wake of a 2018 Royal Commission into the Banking Sector and numerous government interventions, is mortgage lending competitive in Australia? Is the Big 4 as dominant as we think? Is competition for mortgages healthy in Australia? Learn the current state of mortgage lending competition with Savvy’s latest analysis.

- Commonwealth Bank has cornered a quarter of the market

- The rest of the “Big 4” (ANZ, NAB, Westpac) carry 51% share

- 8.57% are “other” non-bank or small bank lenders

- 65% of mortgage holders do not intend to switch mortgage lenders for a better deal

Looking at mortgage lending as a whole in Australia, our previous analysis of mortgages and interest rates shows that mortgage debt has been on a steady increase since 2011, topping out in 2021 at A$2,013.3 billion. As we surmised, this may be due to record low interest rates, government incentives, and a rush to get the jump on rising inflation. Australians love a bargain; and if we can get one on our mortgages, more so the better.

Even so, does that mean Australians are getting a good deal? Is there enough competition in the sector for Australians to have real choice in where they choose to take out their mortgages?

Is there wide competition in the mortgage market, or is it dominated by one or two big players? What about those below the Big 4? Are mortgage holders voting with their feet and switching, now that it's easier? We find out in this analysis by Savvy.

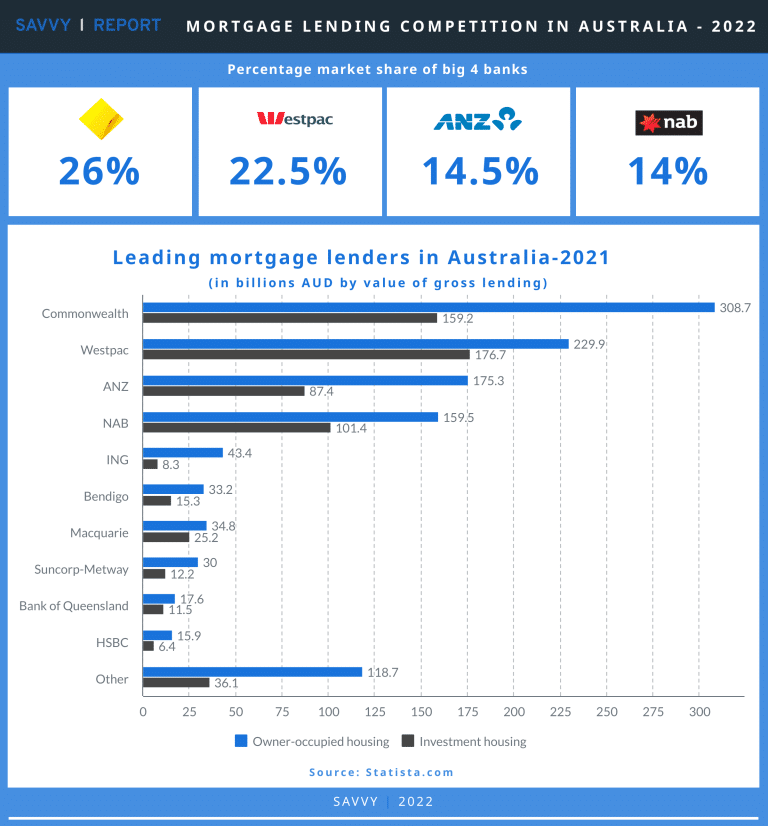

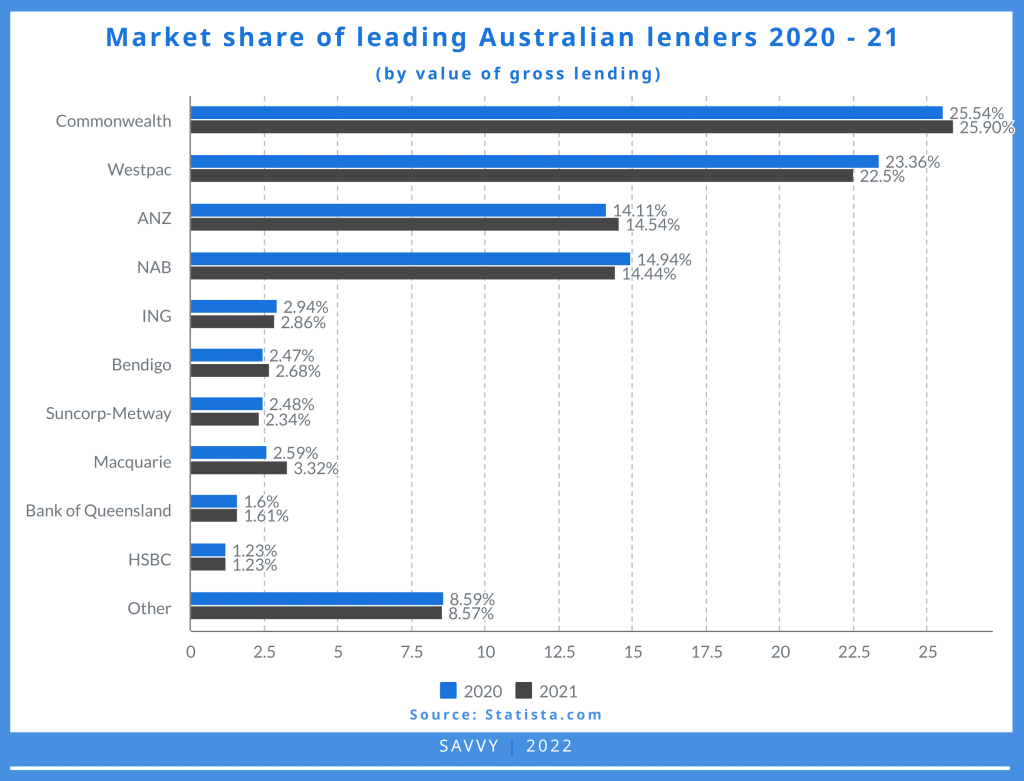

Market share of lenders

According to Statista & APRA, the mortgage lending market as of January 2021 was dominated by the Commonwealth Bank of Australia, which has captured a 25.90% share, up from 25.54% in 2020. Coming in just behind is the Westpac Banking Corporation, on 22.5% down from 23.36% in January 2020. Australia New Zealand Banking Group (ANZ) on 14.54%, up from 14.11% over the period, was slightly ahead of The National Australia Bank (NAB), on 14.44% (down from 14.94%).

The next largest share comes from the “other” category – small credit unions, non-bank lenders, and alternative funding sources at 8.57% (down 0.02% from the previous year.)

One of the biggest movers (at least proportional to their size) is the Macquarie Bank Limited, which climbed from 2.59% to 3.32% of the market. Bendigo Bank similarly increased market share across the January 2020 to 2021 period from 2.47% to 2.68%, while Suncorp-Metway Ltd declined from 2.48% to 2.34%.

https://www.statista.com/statistics/1211594/market-share-of-mortgage-lenders-australia/

Largest mortgage holdings by lender

Unsurprisingly, Commonwealth Bank holds $308.7 billion in owner-occupier mortgages and $159.2 billion in investment mortgages for a total of $467.9 billion.

This is followed by Westpac with $229.9b in owner-occupier mortgages and $176.7b in investment lending – the latter representing 43.5% of their total mortgage lending.

ANZ and NAB are almost on identical figures – ANZ lending $262.7b and NAB $260.9b.

ING Bank seems to favour owner-occupiers, having lent $43.4b versus only $8.3b for investments – a share of only 16%.

The non-Big 4 or “Lower Six” have about $174.9b combined in owner-occupier mortgages – barely even reaching the levels of the Big 4.

The “Other” category holds $118.7b in owner-occupier mortgages and $36.1b in investment housing, a total of $154.8b – almost as much as the “Lower Six” mortgage lenders.

Is it a case of the Big 2 and “Bigger” 2?

As seen in the market share and holdings of the Commonwealth Bank and Westpac, it seems like there is the “Bigger 2” – owning 48.39% of the market – and the “Big 2” of NAB and ANZ on a distant second with a combined 28.97%. The other six major banks comprise only 14.04% of the market. Though financial analysts and commentators regularly refer to ANZ, CommBank, NAB, and Westpac as the “Big Four” banks, it would be more accurate to separate CommBank and Westpac as the “Bigger 2.”

Are we more competitive than other countries?

It would seem that the Australian experience is mirrored in countries with similar financial institutions to ours – such as the United Kingdom.

In the United Kingdom, by comparison, it seems there too is a dominant segment: a “Bigger 2” and a “Big 3” underneath – Lloyds Banking Group capturing 19.7%, Nationwide BS 13.1%, NewWest Group with 11.4%, Santander UK on 11.4%, and Barclays on 9.8%. The UK’s “other” institutions comprise 11.6% market share.

Though it would be a stretch to say the UK is more competitive than Australia, it seems that there are a few natural market leaders and a healthy number of alternatives for those who want to shop around for a better deal on their mortgage.

There is competition – if you want it

The Australian Government banned exorbitant or over-the-top mortgage exit fees in 2011. Other fees such as fees for no service were abolished in the wake of the Royal Commission into the Banking Sector in 2018.

This theoretically encouraged Australians to refinance their home loans with more competitive lenders – but it hasn’t really happened, says Savvy CEO Bill Tsouvalas.

Bill Tsouvalas, Savvy Managing Director & home finance expert;

“According to Statista, only eleven percent of Australian mortgage holders have switched mortgage lenders for a better deal in the last twelve months over 2021,” he says. “What’s incredible to me, having spent the bulk my career in personal finance, is that sixty-five percent of Australians haven’t switched and have no intention to switch.

“This is buoyed by the fact that twenty-eight percent of respondents to that survey said they successfully negotiated a better rate with their current bank or lender, which is a positive sign that banks are aware of the competitive nature of the mortgage market and will attempt to accommodate the needs of their customers.

“I suspect that these naysayers will be eyeing off the market closely as the Reserve Bank moves to increase interest rates to combat rising inflation. Those who can lock in competitive rates now will be in a far better position than those who try to get a better deal after the horse has bolted.”

This information is general in nature and not a substitute for professional financial advice.

Statista.com - Australia Switching Mortgage Lender for a Better Deal

Statista.com - Leading Mortgage Lenders Australia by Value of Lending

Statista.com - Market Share of Mortgage Lenders Australia

Statista.com - Leading Mortgage Lenders in the United Kingdom from 2020 to 2021

RoyalCommission.gov.au - Banking

Did you find this page helpful?

This guide provides general information and does not consider your individual needs, finances or objectives. We do not make any recommendation or suggestion about which product is best for you based on your specific situation and we do not compare all companies in the market, or all products offered by all companies. It’s always important to consider whether professional financial, legal or taxation advice is appropriate for you before choosing or purchasing a financial product.

The content on our website is produced by experts in the field of finance and reviewed as part of our editorial guidelines. We endeavour to keep all information across our site updated with accurate information.